Five things to watch during the Nordic retail Q1 season

Quarterly reporting season is once again upon us. Next two to three weeks will see nearly all major Nordic retailers reporting their results for the first quarter of the year. The market environment is becoming more unstable and unpredictable (again).

Here are five things to watch in this quarter’s results.

1. Price competition in groceries

There has been a lot written about the rising grocery prices. The first quarter results will hopefully give us some indication on which retailers can whether the storm best or even win.

In the UK Aldi and Lidl have started to grow more rapidly after a slight slump during the pandemic. In March Aldi took a strong jump in market share. Today Aldi and Lidl represent a total market share of 15%.

It took 22 years for Aldi and Lidl to reach 10% combined market share. Now they increased that to 15% in six years. And the growth seems to be continuing.

On Thursday Axfood reported it’s Q1 results. They were one of the first signs that the price focused players would become the winners in the new grocery market. Axfood really outperformed the market growth.

Especially Willy’s chain grew faster than the market with 5,4% (market growing by 1,3%).

Also in Finland S-group with stronger price focus of the two big grocers, reported faster than the market growth.

ICA and Kesko are about to report their results next week (ICA on 28th and Kesko on 29th). During the last year both ICA and Kesko have been losing to the market more often than winning the market.

Will this continue or even accelerate as the inflation starts to bite into the customer wallets?

On top of the price pressure, another challenge for grocery retailers’ growth is the resurrecting restaurant sector. After the pandemic restaurants have started to take ever bigger share of customers’ food spend. In the US restaurants’ share of food spend is getting back to pre-Covid levels. In March 50% of all money spent for food was spent in restaurants.

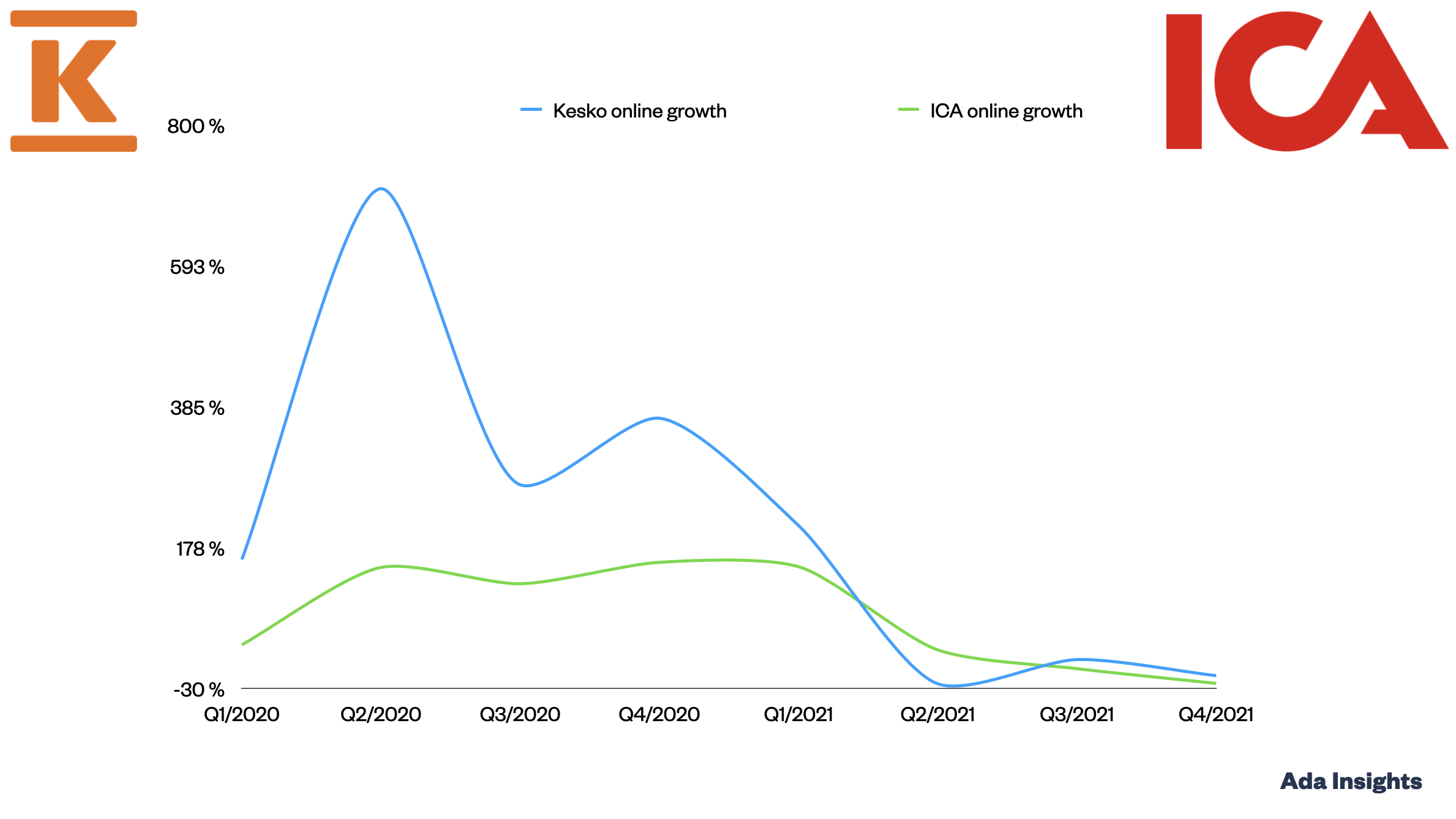

2. Where is online grocery heading?

After two really turbulent years in 2020 and 2021, online grocery market in Sweden seems to be finding a new level from which to continue to grow again.

It will be interesting to see which players have performed above the market and which have struggled to match the market. Of the incumbents reporting quarterly, Axfood performed slightly better than the market.

Year on Year comparisons were negative for both market and Axfood.

However, in absolute revenue terms, online is significantly higher than pre-pandemic.

Of the two grocery giants still to be reporting, it will be interesting to see how ICA and Kesko have performed in the online channel during the first quarter.

Both ICA and Kesko were the big pandemic online grocery winners growing almost explosively during 2020. Since then the growth numbers have come down and during 2021 there was even decline for online.

The plateauing of growth is natural after such dramatic growth periods.

In Finland, S-Group has been gaining Kesko’s lead in the online channel and the companies seem to be on a rather equal level. Another challenge for Kesko’s online growth is Oda’s entrance to Finland. For 2022 Oda will not have notable influence to Kesko’s online channel, but in 2023 will need to step up its online game, especially in Helsinki region.

However, Q1/2022 has been the first full quarter for the new Ocado fulfilment center in the greater Stockholm region. Thus, one could imagine that ICA has a big desire to drive volume to online in order to get the warehouse operating as efficiently as possible.

3. DIY: will the strong growth continue?

DIY has been one of the best performing sectors within retailing. In Sweden the industry received a significant Covid bump in 2020 and managed to grow on top of that in 2021. Same happened, albeit on a bit smaller scale, in Finland

Byggmax kicked off the reporting season with a strong 14% revenue growth. The bigger Nordic DIY retailers K-Rauta and BHG will be reporting their results during the next week. Both of the companies had a strong year in 2021.

BHG continued its strong growth trajectory with a 40+% growth in 2021. The faster growing segment for the company was Home Furnishings, which grew by 63% as a result of three major acquisitions. Organic growth for the Home Furnishings segment was 8%.

On the other hand the DIY segment grew by 28%, of which 14% was organic growth. In total already 43% of revenue at the BHG group is coming from the Home furnishing.

K-Rauta has been relying much more on the business to business sales in it's growth. Onninen has been an important growth driver for K-Rauta. Currently Onninen represents almost half of all DIY sales at Kesko.

Can Kesko DIY keep it’s robust growth? With the current growth path continuing, maybe the DIY segment could eventually challenge groceries as the biggest segment within Kesko?

4. More success for the discount retailers?

Discount retailing in the non-food sector was another category that flourished during the pandemic. In the Nordics Tokmanni and Europris represent two big and publicly listed companies. Both of them have grown fast over the last six years and particularly fast during the last two years.

Especially Europris had a stroing pandemic time with a 40% growth from the pre-pandemic 2019 revenue levels.

The growth has stabilised significantly for both companies, briefly even dipping into decline. However, the profitability of both companies have remained good.

It will be very interesting to see how these two companies can a) sustain growth after rapid growth and b) manage costs.

As the inflation starts to bite the consumers' wallets, one could imagine that the discounters would be well placed to grab bigger share of the market.

5. Verkkokauppa.com - how steep will the decline be?

Over the last years Verkkokauppa.com has grown steadily as a result of customers transitioning to buy things online. However, Verkkokauppa.com also declined more rapidly as the societies started open up after the pandemic. During the last quarter of 2021, Verkkokauppa.com saw sales decline.

According to the company, the decline was a result of tough comparison numbers from the previous year. However, in March the company issued a profit warning stating that the revenues for this year would end up some 5% below the 2021 numbers. The reason given was the uncertainties in the marketplace, especially due to the war in Ukraine. It certainly seems that the war has had some (at least short term) impact on the online retail market in Finland.

However, interestingly in Q4/2021 Verkkokauppa.com saw bigger revenue drops in the bricks and mortar stores than for online. It will be interesting to see whether the stores have been declining more during the first quarter or whether online has been the channel suffering more.

It would also be interesting to understand how the different categories of Verkkokauppa.com have developed.