Member loyalty driving top line growth at Costco

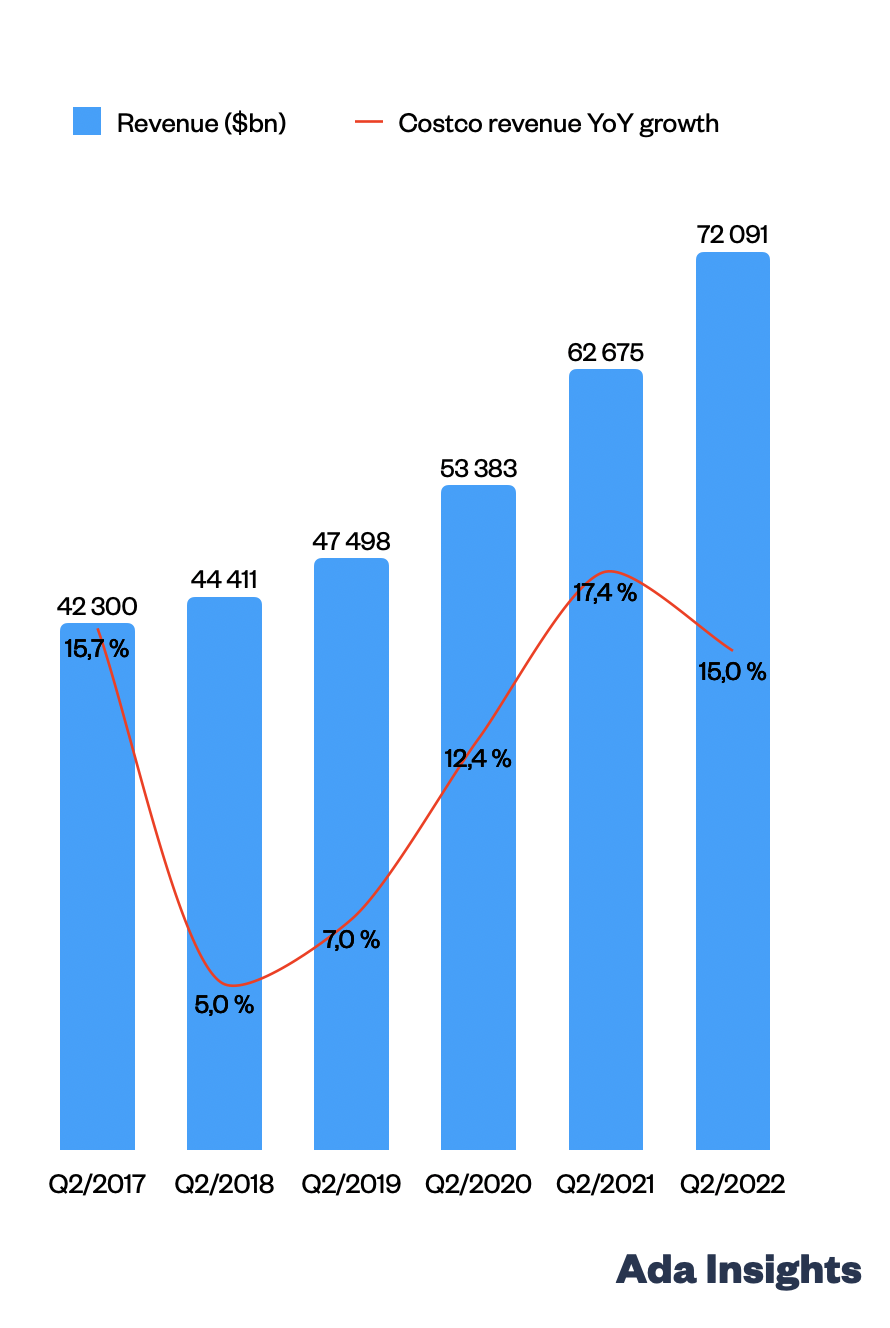

Executives at Costco like to reiterate that they are a “top-line company” that focuses on driving customer loyalty above else. The most recent fiscal Q4/2022 earnings report highlighted this.

The company grew its net sales by 15,2% and memberships by 7,5%. For years (even decades), Costco has reported solid growth figures. The growth has spanned both downturns as well as strong economic growth.

Costco reported an admirable 92,6% renewal rate for their memberships in the US and Canada.

Costco has for decades had 90+% renewal rates. They indicate ferocious loyalty from the customers towards the business model offered by Costco.

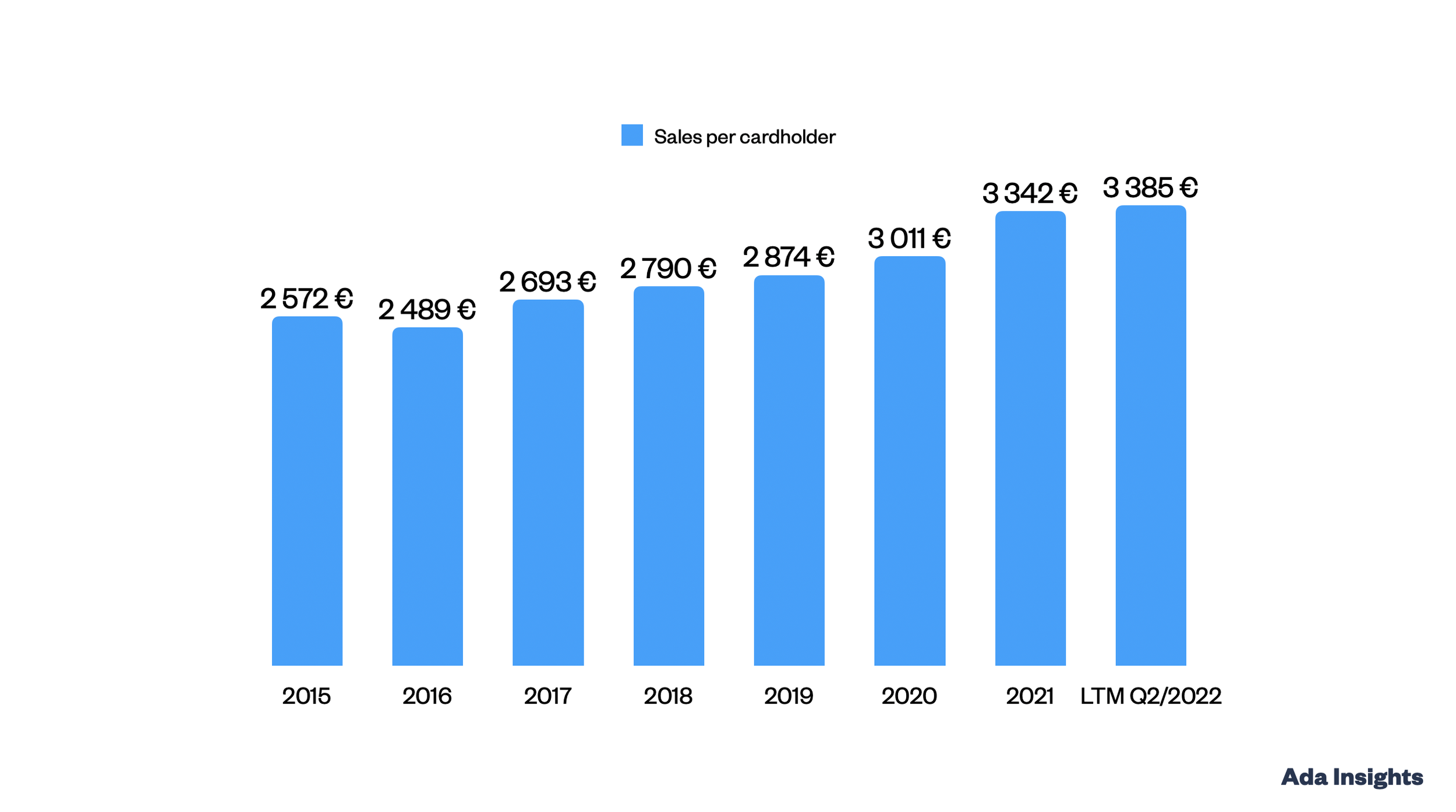

The membership base has grown and become more profitable for the company. Since 2015, the number of paid cardholders has increased by 47,5%. At the same time, the sales per cardholder have grown by 31,6%. The growing sales per cardholder mean that Costco has significantly increased its revenue per customer. Coupled with strong loyalty, this is a sign of a strong company.

Comparing the Sales, General & Administrative costs relative to the Net sales illustrates the uniqueness of the Costco model (and part of its lure for the customer). Costco has a much smaller share of revenue going to salaries, marketing and other administrative costs than its main rivals.

Increasing inventory is not a problem for Costco

Inventories have been a hot topic in retailing over the last six months. Costco has seen its inventories by 26% year over year. For Costco, inventory is not a similar problem as it is for some of its competitors. Firstly, Costco relies heavily on food, which turns over rather rapidly. Secondly, Costco’s narrow assortments make high inventory turnover easier to achieve. And thirdly, the top line growth at Costco tends to alleviate growing inventory as it is purchased faster by the customers.