Big retailers driving growth in Finnish retailing in Q3

As the major retailers have reported their Q3 results, it is time to reflect upon how the late summer and early autumn have progressed in retailing in Finland.

The big picture of the sector is that the retail industry has recovered from the pandemic rather well.

As a whole the industry has grown from both pandemic (Q3/2020) as well as the pre-pandemic levels (Q3/2019). Since last year the industry has grown by almost 5%. This time the industry growth has been led by non-food sectors, whereas during the pandemic grocery retailers were the ones driving the growth.

Because of the big proportion of sales going through the two giant grocery retailers (S-Group & K-Group), the entire sector performed quite well throughout the pandemic.

The only bigger part of retailing that has not been able to achieve pre-pandemic levels of sales is the clothing sector.

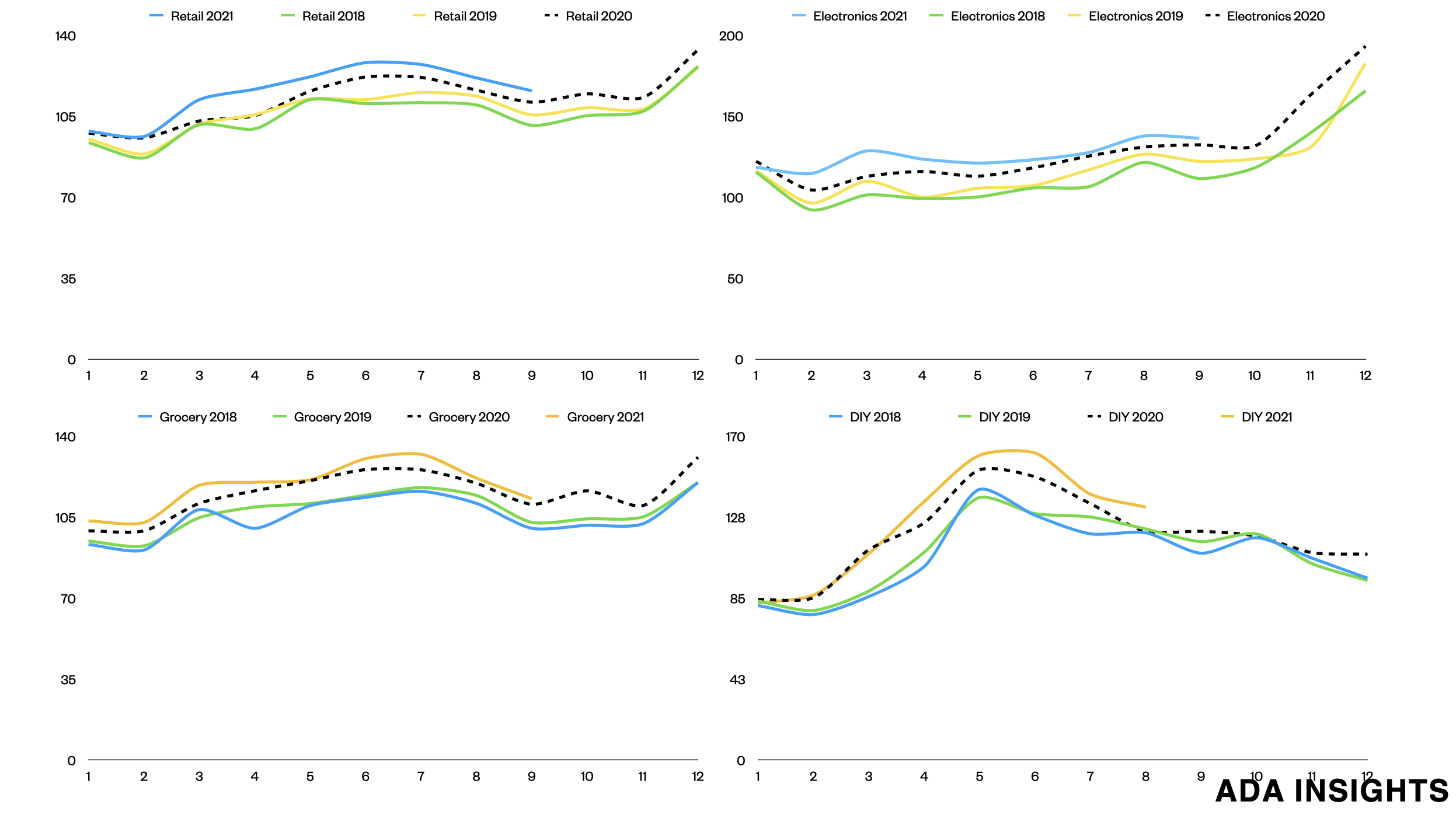

Monthly development of certain retail sectors (Source: Statistics Finland)

As the image illustrates, during the spring of 2020, the retail industry only briefly dipped below 2019 levels. Since then the industry has kept on growing. The four sectors illustrated in the image above all saw very positive sales growth throughout the pandemic and have been able to sustain the elevated sales levels during 2019.

Alongside groceries, DIY has been sector enjoying remarkable sales growth as a result of people spending more time home and subsequently more money for renovating and decorating homes.

Monthly development of certain retail sectors (Source: Statistics Finland)

Whereas the biggest sectors of retailing flourished, some other parts of the industry struggled. Home and Sports/other sectors dipped heavily at the start of the pandemic, but have since recovered well above the 2019 levels. As mentioned earlier Clothing has not been able to recover.

Besides Clothing another sector that has in many countries seen severe declines are the Department stores. In Finland Department stores saw declining sales, but along many other sectors, recovered rapidly. However, this is not a totally straightforward illustration of the sector.

Much of the growth of Department stores has been coming from the Non-food sales of the big Hypermarket chains, as well as from Tokmanni.

The two big department store chains, Stockmann & Sokos, had a very difficult year in 2020. Sokos’s revenue declined by 19% and Stockmann even worse sales development.

However, Stockmann has seen growth during 2020. One can assume that Sokos has also been growing during this year. However, despite strong growth in Q3/2021 Stockmann sales are still trailing the 2019 levels.

Big retailers growing rapidly

From the Q3/2021 reporting one can derive that the big retail chains are performing very solidly after a year of big growth. The big winners of the pandemic, hypermarkets & Tokmanni, have been replaced by Verkkokauppa.com, K-Rauta & Musti Group.

To be honest, Musti Group has been one of the best performing retailers all along the last two years.

Verkkokauppa.com has been growing sales steadily during the period. Unfortunately we don’t have official online sales statistics in Finland, like in other countries. It would be easier to see whether Verkkokauppa.com has been outperforming the market in general.

Online grocery growing after extraordinary 2020

For online grocery, the market has kept on growing, but naturally much slower than in 2020. As Kesko was the fast growing online grocer of 2020, S-Group seems to have catched up Kesko during 2021. This would imply that S-Group has also already reached in nine months of 2021 the online grocery sales level that they had during the entire year 2020. On the other hand, Kesko is approximately 70-75% of the way to 2020 levels of sales.

With these sales developments, one could estimate that the online grocery market could reach around 450-500 M€ from the two big retailers.

With the small challengers added to that, the market could end up somewhere between 500-550 M€ for 2021.

That would give 25-35% annual growth from the extraordinary 2020.

S-Group gaining K-Group in groceries

Besides the online channel groceries, S-Group seems to be gaining K-Group in offline grocery sales also. Since the start of the year, K-Group has grown less than the market six out of nine months. During the Q3, K-Group sales were very slightly below the market growth. This was driven by slight growth miss from the hypermarkets (Prisma winning over Citymarket) and big supermarkets (probably driven by the growth of S-market).

The very slight market share gains from S-Group are probably a result of store renovations/refurbishments that have been rolling out over the last years.

These results are starting to come out for the coming years. Also the more rapid growth of online grocery could help slightly S-Group to etch out an advantage in the market.

It will be very interesting to follow how the competition unfolds over the Christmas quarter for the big grocery retailers as well as for the recovering clothing retailing. Is Stockmann finally on a path to a more solid footing?