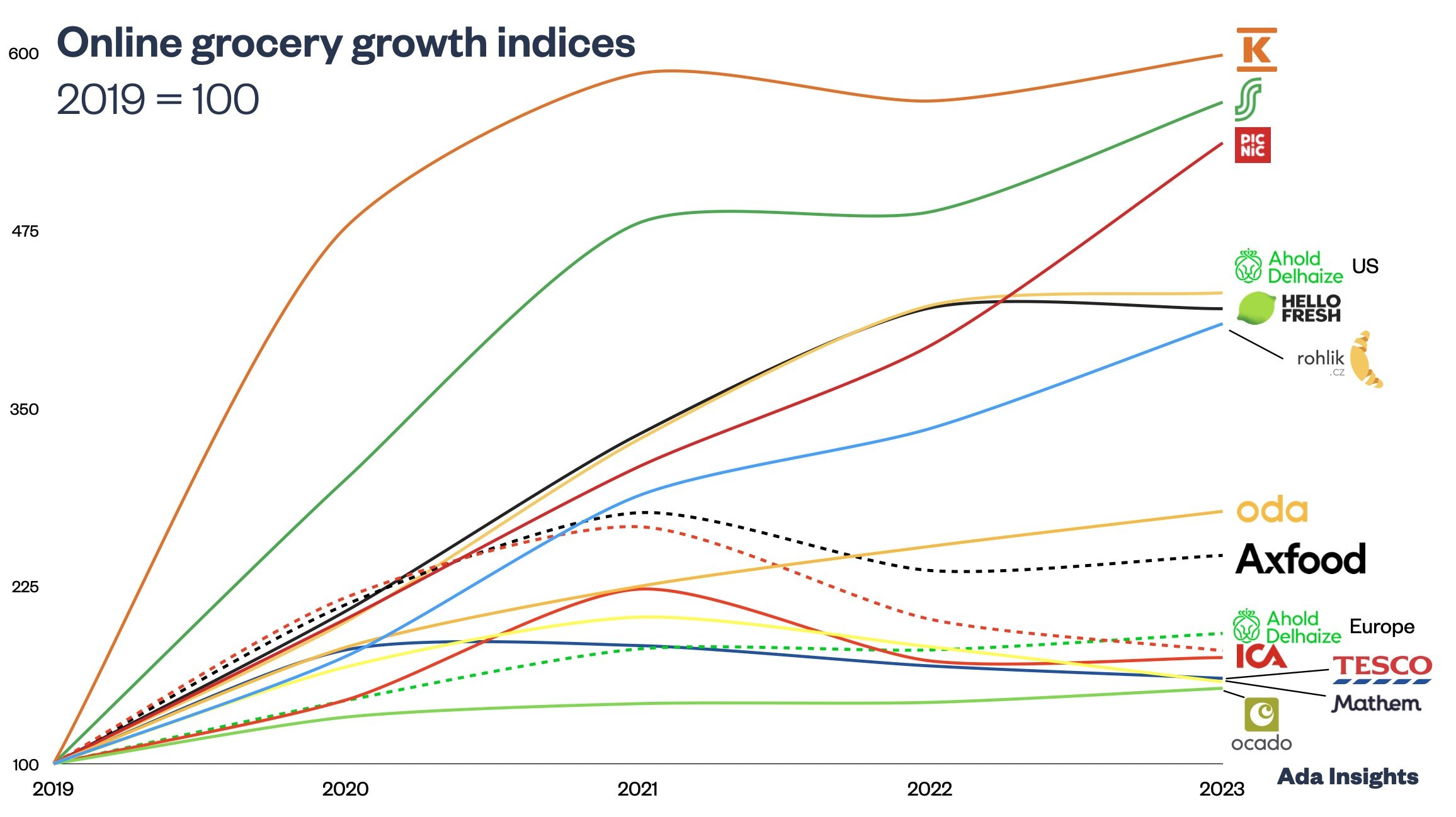

HelloFresh continues fragile growth momentum with improved profitability

Meal-kit company HelloFresh reported a second consecutive quarter of revenue growth, with a slight increase of +1,7%. However, the company has seen its share price plummet due to the slowdown in revenue growth during 2023, when revenue declined for three quarters.

The slight rise in revenue is shadowed by the seventh straight quarter of declining order numbers. Revenue grew because the company has been able to consistently increase its Average Order Values (AOV).

Only once has the AOV declined in the last 24 quarters. It is already 37,5% higher than pre-pandemic (Q2/2019).

With improving revenues and tight cost control (fulfilment and marketing costs grew less than revenue), HelloFresh has improved profitability. Both AEBITDA and EBIT margins improved. Also, the Free Cash Flow produced by HelloFresh increased by 34% to 51 M€.

This is despite declining gross margins. According to the company, the margins decreased because of the rapid growth of the Ready-To-Eat (RTE) segment. RTE has higher costs than meal kits.

“Meal kits is our original, largest, and most profitable product category. However, it has represented the biggest drag on our financial performance in recent times, with both revenue and margins failing to meet our expectations of a couple of years ago.”

The main business segments of meal kits, representing more than 70% of the business, declined 9,3%. This was countered by the rapid growth of the RTE business (+46,7%). Currently, RTE generates more than 25% of HelloFresh's revenue.

However, the company has quickly built the RTE business into a two billion euro run rate business. As the meal kit business has faltered, this provides a great growth lever for the company.

“Unlike meal kits, our RTE product category has surprised on the upside when it comes to demand growth. In less than 4 years since acquiring the then small RTE brand Factor, our RTE product category has grown by nearly 20x. In 2024, our RTE product category will be both larger and more profitable than the entirety of our Group was before the pandemic”